Summary

The recent run-up in revolving debt combined with the much higher financing costs raises doubts about the ability of credit to continue to make up for the shortfall between modest real income growth and aspirational spending. Is there a way to feel better about the consumer credit situation?

How long can consumers brush off higher rates?

The economic story of the year so far is how hopes for lower interest rates have been dashed by a disruption in the trend decline in inflation. The gravity-defying power of consumer spending deserves a hearty share of the blame. Unbroken by the highest cost for consumer credit in decades, it is difficult to look at spending today and find indications of a consumer that is chastened by higher financing costs. But with pandemic-era savings now fully depleted, bridging the gap between aspirational spending and comparatively modest real income growth, consumers are running out of options. This report unpacks the latest data on consumer credit with a skeptical eye on the ability for consumers to keep borrowing.

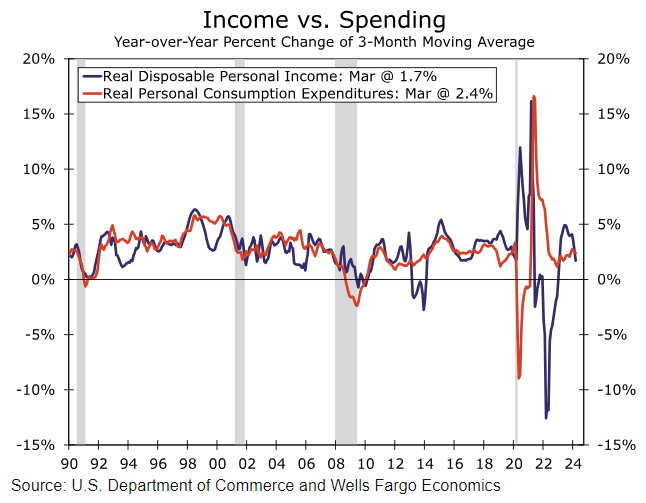

Spending and income, the broken relationship

On an inflation-adjusted basis, consumer spending tracked reasonably well with disposable income growth in the 20 years leading up to the pandemic. In overly simplistic terms, more income meant more spending. Things got turned upside down over the past four years (Figure 1). Beginning during the quarantine and early pandemic years the linkage between these series broke down. Initially income soared amid generous fiscal stimulus programs as spending was cut way back. Then inflation generally outpaced income growth as real disposable income cratered, yet spending roared ahead facilitated by stashed cash and easy access to relatively cheap credit.

Download The Full Special Commentary

Analysis feed