- Expectations of earlier but shallower Fed rate path revive optimism

- Dollar retreats, stocks and gold recover as long-dated yields drop

- China’s factory prices soar, central bank speakers in focus

Fed repricing

Investors are having second thoughts about the structure of the Fed’s rate hike cycle. The latest moves in the bond market suggest the FOMC will pull the hike trigger early to tame inflation but the final destination in rates won’t be very high. In other words, an earlier but shallower rate path.

This is evident by the yield curve flattening, with short-term Treasury yields rising yesterday while longer-term yields fell after the release of US inflation data and the minutes of the latest Fed meeting. Inflation remained hot with consumer prices rising 5.4% in yearly terms, chipping away at the ‘transitory’ narrative as price pressures seem to be broadening out.

Meanwhile, the minutes revealed that the Fed is planning to reduce its asset purchases by $15bn per month, starting in mid-November or mid-December. In fact, ‘several’ participants indicated they would prefer an even faster pace. However, this group probably includes Kaplan and Rosengren who have already left the FOMC, so the hawkish signal should be taken with a pinch of salt.

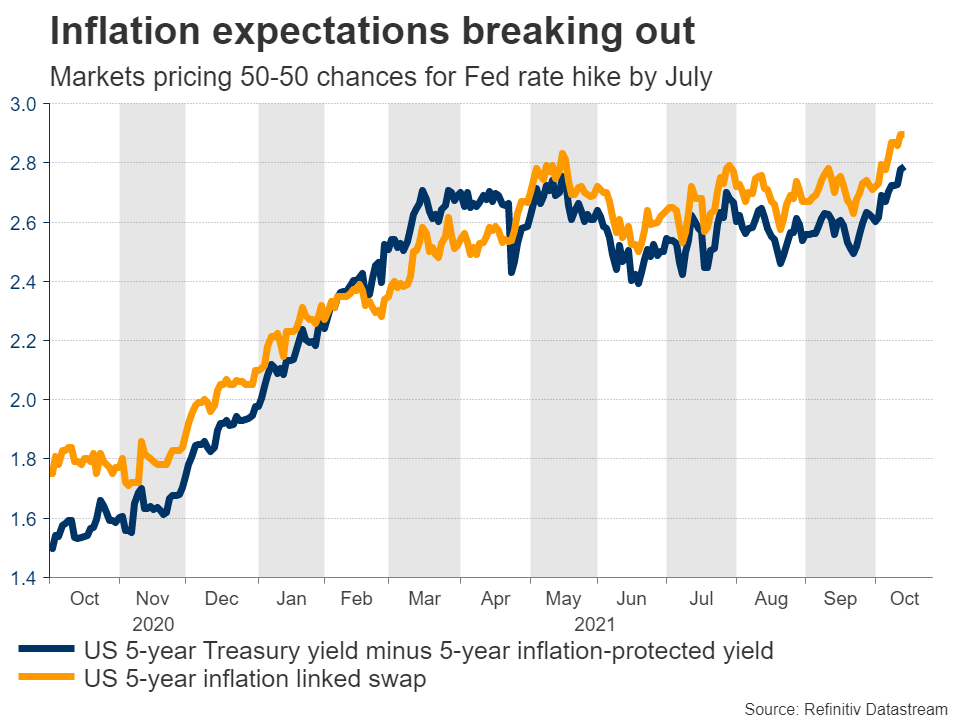

Inflation expectations have moved higher since this meeting thanks to the meteoric rise in energy prices, so markets concluded the Fed may be forced to tighten earlier to break this spiral, although its early actions imply rates won’t need to rise too high overall. Another explanation is that investors think any premature tightening will ultimately backfire.

Inflation expectations have moved higher since this meeting thanks to the meteoric rise in energy prices, so markets concluded the Fed may be forced to tighten earlier to break this spiral, although its early actions imply rates won’t need to rise too high overall. Another explanation is that investors think any premature tightening will ultimately backfire.

Optimism returns

In the markets, the drop in longer-dated yields overshadowed everything else, breathing life back into equities and gold prices. Yield-sensitive tech and growth stocks benefited the most as traders grew more confident that the Fed won’t risk a repeat of the late-2018 market crash, which was triggered by rates rising too far.

The optimism has carried over into today’s session, with Wall Street futures pointing to another positive open. That said, the technical structure still argues for caution as the S&P 500 and the Nasdaq have been unable to record a higher high yet, even if ‘stagflation’ worries have taken a back seat. There’s also a barrage of earnings releases coming up from Bank of America, Citigroup, Wells Fargo, and Domino’s Pizza.

Gold capitalized on the drop in longer-dated yields and the pullback in the dollar, shooting higher to meet resistance near its 200-day moving average. If yields continue to ease as traders bet that the terminal Fed rate will be lower, that would be fertile ground for bullion to extend its latest gains.

However, any such gains should be viewed as a rebound within a broader downtrend, not a trend reversal. Inflation expectations keep grinding higher along with oil prices, so inflation worries could return at any moment to drive yields higher. In a sense, gold is at the mercy of the bond market, which in turn remains at the mercy of the volatile energy market for now.

Dollar eases, loonie climbs

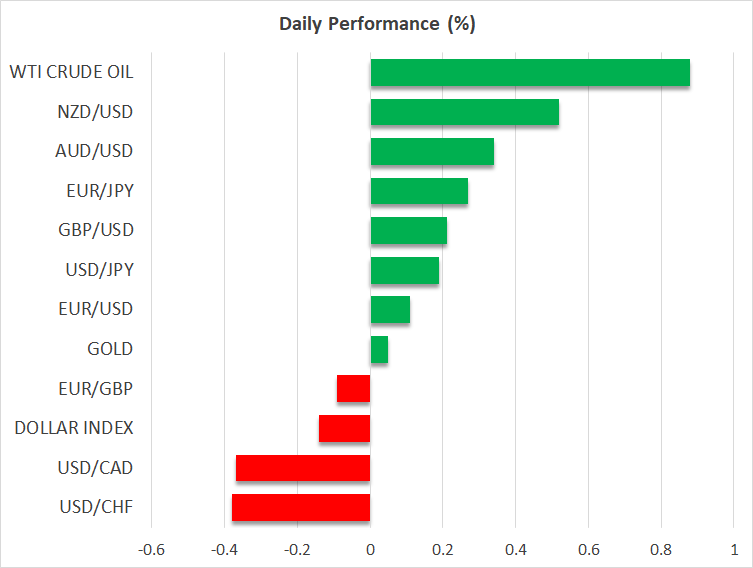

In the FX spectrum, the dollar suffered some minor injuries from the latest gyrations in yields, although the yen has been much weaker this week. The main beneficiaries have been the commodity-linked currencies, and especially the Canadian dollar that is riding the rally in oil prices.

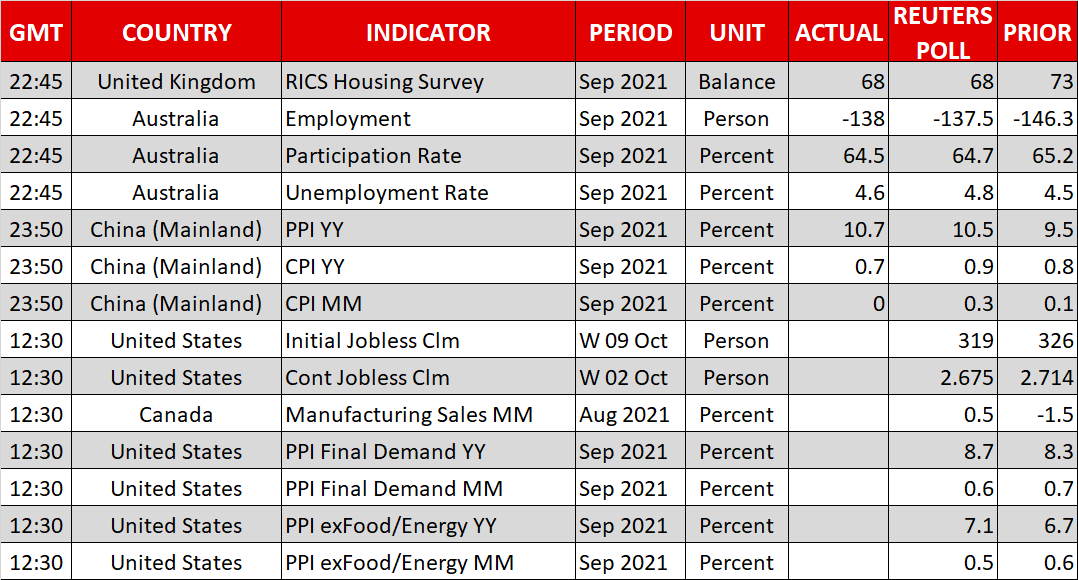

Meanwhile, the inflation story will remain front and center today with the release of US producer prices. China’s own factory prices accelerated to 10.7% in yearly terms according to data released overnight, feeding concerns that the nation will begin exporting even more inflation abroad.

Finally, there’s also a central bank charm offensive on the agenda. We will hear from the Bank of England’s Tenreyro (10:10 GMT) and Mann (14:40 GMT), while across the Atlantic, the Fed’s Bullard (12:35 GMT), Bostic (14:00 GMT), Daly and Williams (both 17:00 GMT) will deliver remarks.

Thursday, 14 Oct, 2021 / 9:47