· Stocks slip as traders cut exposure to tech and pre-profit companies

· Dollar unable to capitalize on the risk aversion amid inflation worries

· Cable stabilizes after sprint higher, Fed speakers in focus today

Dash for value continues

Dash for value continues

Wall Street came under pressure at the start of the new week as the rotation away from growth and tech stocks escalated. While the overall stock market is still near record highs, tech investors are quietly heading for the exits and early-stage companies without profits have been annihilated.

There isn’t a clear catalyst behind this purge. It seems to be a combination of inflation fears making a comeback and some market participants moving higher along the value spectrum, cutting their exposure to anything with a stretched valuation.

That said, the fact that the selloff has been mostly isolated to the tech and growth spheres is quite encouraging, as it suggests that investors haven’t lost faith in the economic outlook but are merely moving away from more speculative plays. Indeed, this correction could even calm some ‘bubble’ concerns, considering what is being sold.

Overall, it’s doubtful that this selloff will last long in an environment where the Fed is still going a hundred miles an hour and federal spending keeps flowing as the economic crisis fades into the rear-view mirror. Bonds are still a dead asset class and commodity markets are too small, so there’s simply no alternative to equities.

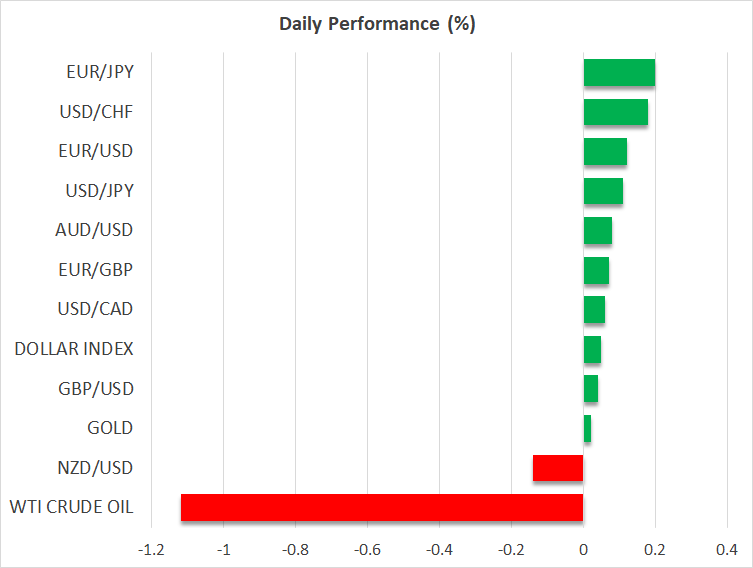

Dollar languishes as inflation expectations edge higher

In the FX theater, the US dollar was unable to gather much support from the latest bout of risk aversion and continues to bleed early on Tuesday even as futures point to another negative open on Wall Street.

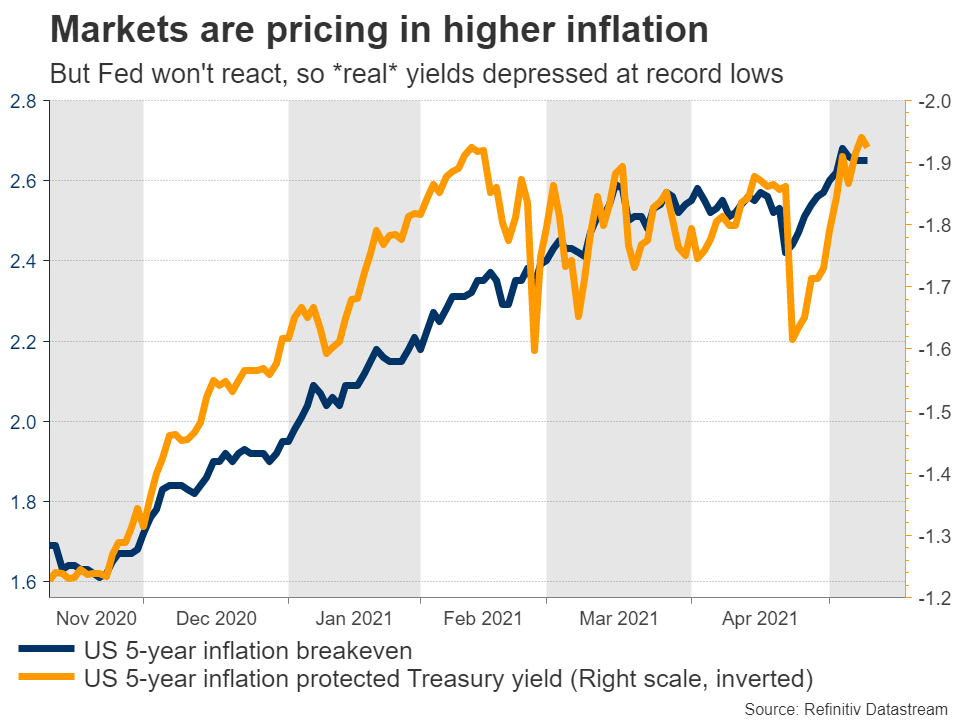

The reserve currency’s inability to gain any traction seems linked to inflation dynamics. Market-based measures of inflation expectations have been moving higher with speed lately as traders try to keep pace with the electrifying boom in commodity prices, from lumber to copper to corn. Meanwhile, Treasury yields have stuck to their recent range, pressuring real yields.

With the Fed doubling down on its promise not to react to an inflation episode and mounting signs that cost-push inflation is indeed imminent, real yields could remain depressed and the summer months could be a tough period for the dollar. Even though the greenback’s ultimate trajectory still seems positive, the shockingly disappointing jobs report has likely pushed back the Fed’s tapering discussion, delaying any dollar strength until later in the year.

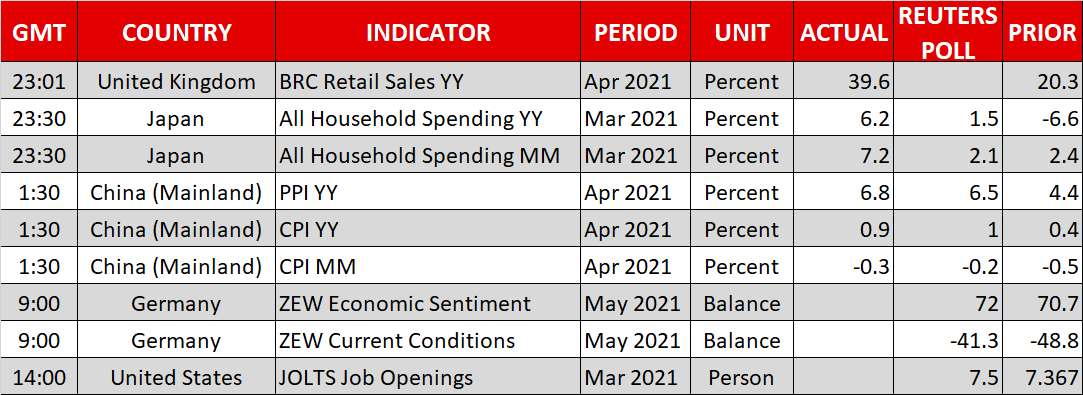

For now, markets are waiting with bated breath for tomorrow’s CPI inflation data for the next clue in this puzzle.

Sterling sprints higher, Fed speakers in focus

So the dollar may struggle for a while, but against what? The Eurozone is still in dire straits economically and Japan’s vaccination rollout has been excruciatingly slow. The answer might lie with Britain and Canada.

The British and Canadian economies are doing much better and vaccinations have been impressive in the UK especially, leading the central banks of England and Canada to take baby steps towards ultimately normalizing monetary policy. In this sense, pound/dollar and dollar/loonie might be better proxies for any short-term dollar weakness than euro/dollar or dollar/yen.

As for today, the economic calendar is light but there are a few speeches on the agenda that markets could pay attention to. Bank of England chief Andrew Bailey will participate in a panel discussion with New York Fed President John Williams at 14:30 GMT, while Fed Board governor Lael Brainard will deliver remarks at 16:00 GMT.

XM.COM Review

Tuesday, 11 May, 2021 / 9:26