- Stock markets edge lower after US retail sales disappoint

- Risk aversion reawakens the dollar ahead of Fed minutes today

- RBNZ says rate hikes ‘delayed not derailed’, kiwi goes wild

Stocks bleed, but not much

Stocks bleed, but not much

It was a lively session across global markets. Wall Street came under pressure on Tuesday after US retail sales fell short of expectations, amplifying concerns that consumer spending may be rolling over and reinforcing the narrative that economic growth has already peaked.

Of course, the retreat was mild and there wasn’t any sense of panic selling, with the S&P 500 losing just 0.7%. It is quite impressive that US markets are still within touching distance from record highs, defying an imminent withdrawal of Fed liquidity as well as a worsening Delta outbreak in America and Asia, even with valuations being so stretched.

This resilience might boil down to expectations that the Fed will be infinitely cautious in reining back stimulus and that Congress will put a floor under economic growth by delivering another multi-trillion round of spending. Monetary policy will still be super-loose after tapering and the fiscal taps aren’t closing.

Stock markets can always bleed, but dip buyers aren’t going away anytime soon.

Dollar stands tall, looks to Fed minutes

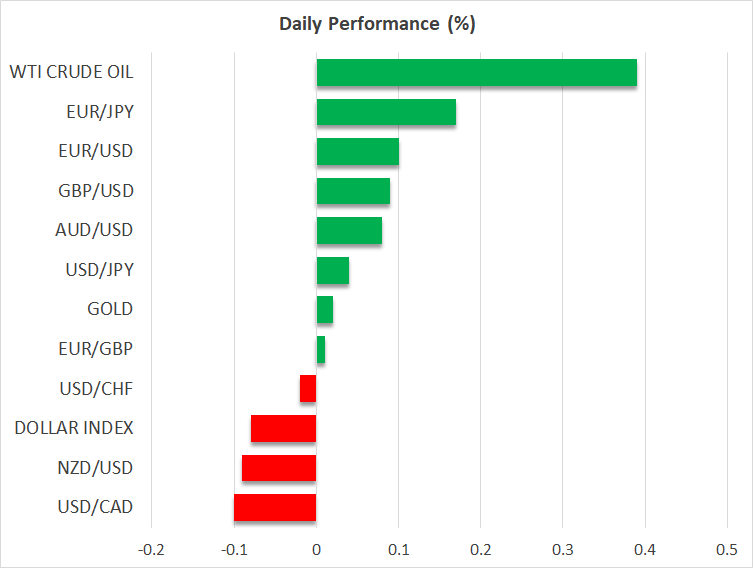

The FX market traded exactly as one would expect when growth worries are the dominant theme, with commodity currencies getting blasted alongside the risk-sensitive British pound.

Across the risk spectrum, it was the dollar that shined the brightest even despite the disappointing US retail sales, highlighting once again that ‘when the going gets tough’ everyone seeks shelter in the world’s reserve currency. The yen also performed well, but its advance was capped by global bond yields rising a little.

Euro/dollar is currently testing its lows for the year around $1.17 and whether it manages to pierce through this region might depend on what the Fed minutes have to say about tapering today at 18:00 GMT. That said, the Jackson Hole symposium next week is where any real hints will drop, so this might steal the thunder from the upcoming minutes.

The question is whether we will get a formal taper announcement in September or November. That doesn’t matter much in the big picture. Tapering is coming, it’s just a matter of time. Even the Fed’s arch dove – Neel Kashkari – said so yesterday. The path of least resistance for the dollar still seems higher, especially against low-yielders like the euro and yen.

RBNZ holds rates, kiwi goes for a rollercoaster ride

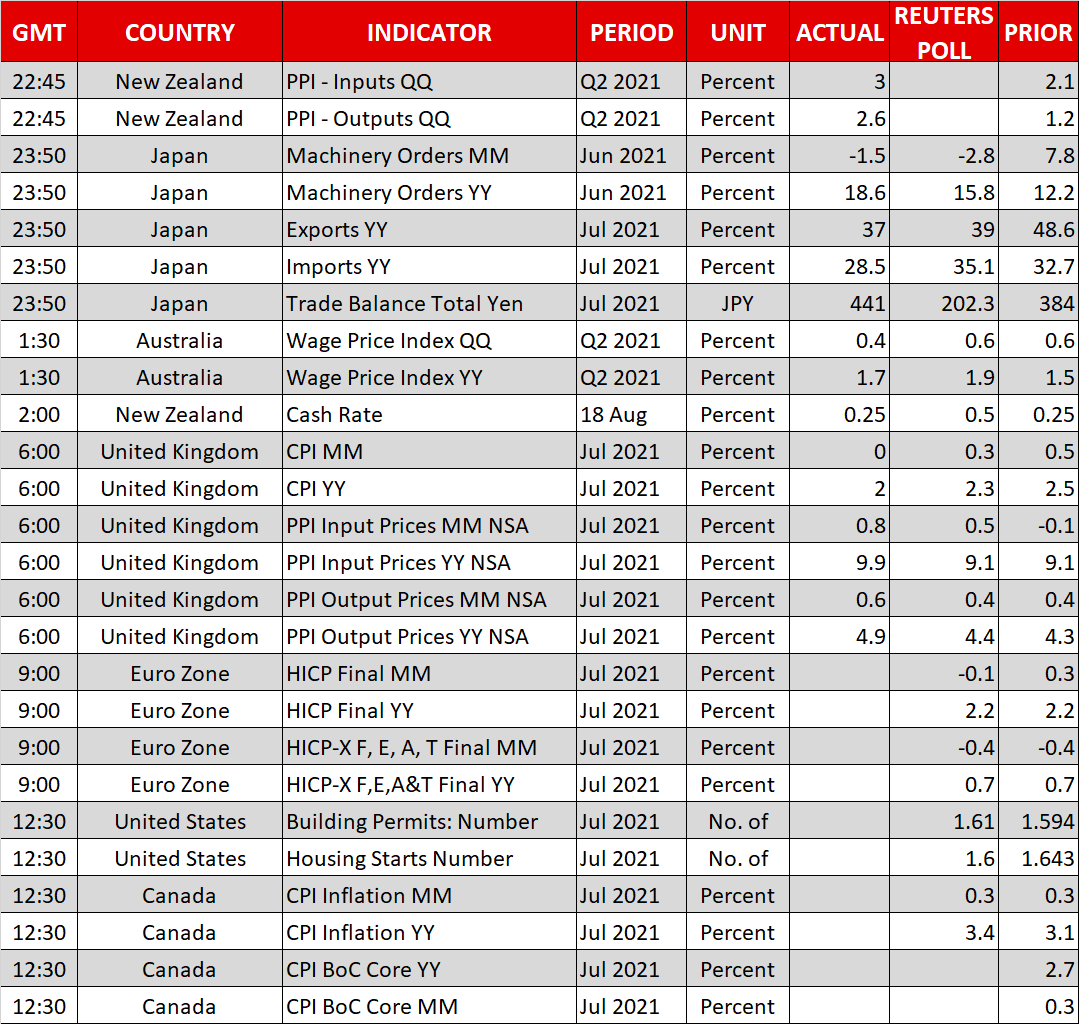

The real fireworks today were in the kiwi after the Reserve Bank of New Zealand kept interest rates unchanged. What looked like a certain rate increase until a couple of days ago was thrown under the bus after the nation went into a snap lockdown yesterday to battle the first virus outbreak in months.

The kiwi took some damage as the RBNZ held its fire, but it came back roaring as Governor Orr signaled that their normalization plans were merely delayed, not derailed. Rate forecasts were revised higher to reflect that, now penciling in around five rate hikes by the end of next year.

Overall, the message was that this isn’t a game changer, but merely a speed bump in the road towards higher rates. The kiwi’s fortunes are now tied to the domestic health situation. Will New Zealand eradicate the virus from its borders again or will it follow Australia in a vicious lockdown spiral? That will determine whether the RBNZ honors its promises.

XM.COM Review

Wednesday, 18 Aug, 2021 / 9:02