-

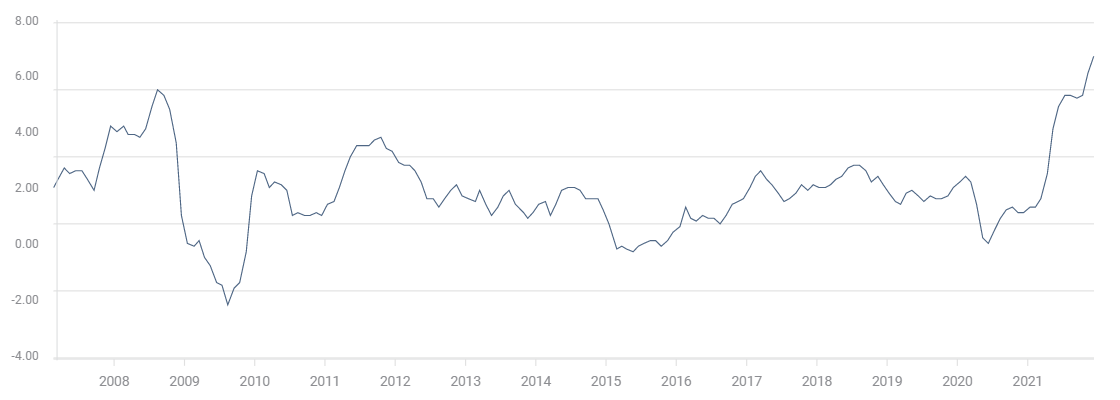

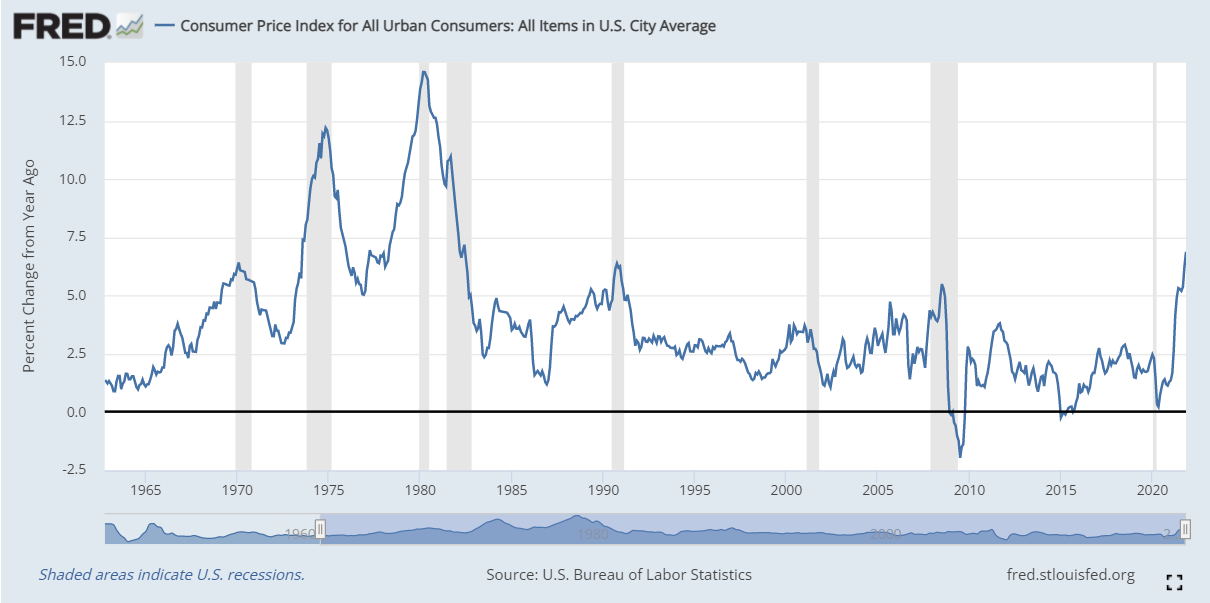

Headline CPI vaults to 39-year high at 6.8%, core at 4.9%.

-

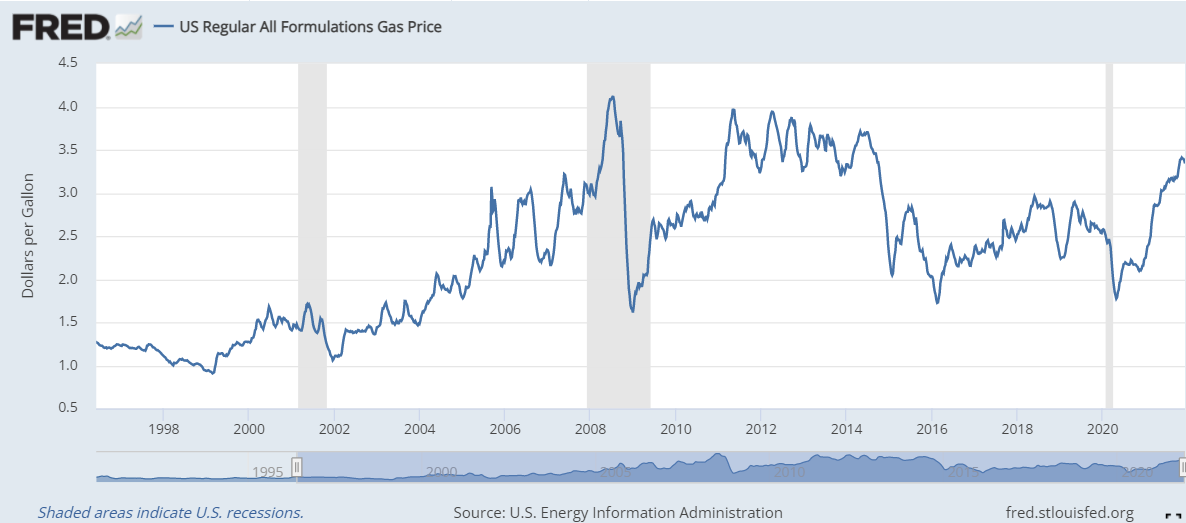

Food prices up 6.1% in a year, energy 33.3%, gasoline 58.1%.

-

Consumer inflation may prompt a wage-price spiral.

-

Federal Reserve accelerated taper expected next week.

Consumer prices rocketed at the fastest rate in almost four decades in November, with gains in necessities from food and gasoline to shelter and cars, leaving little place to protect the family budget.

The Consumer Price Index (CPI) rose 6.8% from a year ago, up from 6.2% in October, reported the Labor Department on Friday. It was the highest inflation rate since 7.2% in June 1982. The core index, minus food and energy costs, jumped 4.9%, accelerating from 4.6% in October and this measure’s largest annual gain since June 1991. Monthly increases were 0.8% for the overall index and 0.5% for core.

CPI

FXStreet

Prices increased for many purchases at the heart of family finances. Food costs are up 6.1% on the year with many common items, like eggs up 8%, bacon up 21%, steak up 24.6% and coffee up 7.5%, even more expensive. The wider category of groceries rose 6.4%.

Energy prices climbed 3.5% in November and are 33.3% higher on the year. Electricity and utility bills were up 11% over 12months. Gasoline, an absolute necessity for most Americans, has soared an astonishing 58.1% since last November. Used car and truck prices are 31.4% higher, their largest annual gain on record, largely on the component induced shortage of new vehicles.

The combined increase in food and energy prices was the steepest in 13 years, according to the Labor Department.

The cost of shelter, a government category that covers rental and home ownership, and is about one-third of the price index, rose 3.8% for the year for the most dramatic gain since the 2007 lead into the housing crisis.

American Consumer prices have now increased 5% or more for seven straight months. That is the longest string since August 1992 to February 1993, a record that will be easily surpassed in December and for months into the New Year. Before that inflation outburst in the first Clinton administration, history returns to the great post-war inflation surge that saw inflation maintained continuously over 5% for nearly a decade, from April 1973 to October 1982.

Markets

Equities were generally receptive to the inflation figures, likely relieved that the annual numbers were exactly in line with expectations.

The Dow added 0.61%, 216.63 points to 35.091.21 and is within 1.6% of its all-time record from November 8 at 36,565.73. The S&P 500 rose 44.57 points, 0.95% to close at a record 4,712.02, a mere 31 points from its top at 4.743.83.

S&P 500

CNBC

Credit markets were more circumspect as they await the Fed’s December 15 meeting. The 10-year yield was unchanged on the day at 1.487% though it was 13 basis points higher on the week. The 30-year bond yield was 2 basis points to the good at 1.889% on Friday and it has gained 20 points on the week.

The US dollar was modestly lower in the major currency pairs, with similar logic that inflation was not worse than expected.

-637747729176253483.png)

-637747729314488993.png)

Markets have priced in a doubled taper to $30 million monthly and a conclusion to the bond program about the middle of March, for the Wednesday Federal Open Market Committee (FOMC) meeting. The Projections Materials are expected to show two fed funds rate increases in the second half of next year.

Real wages

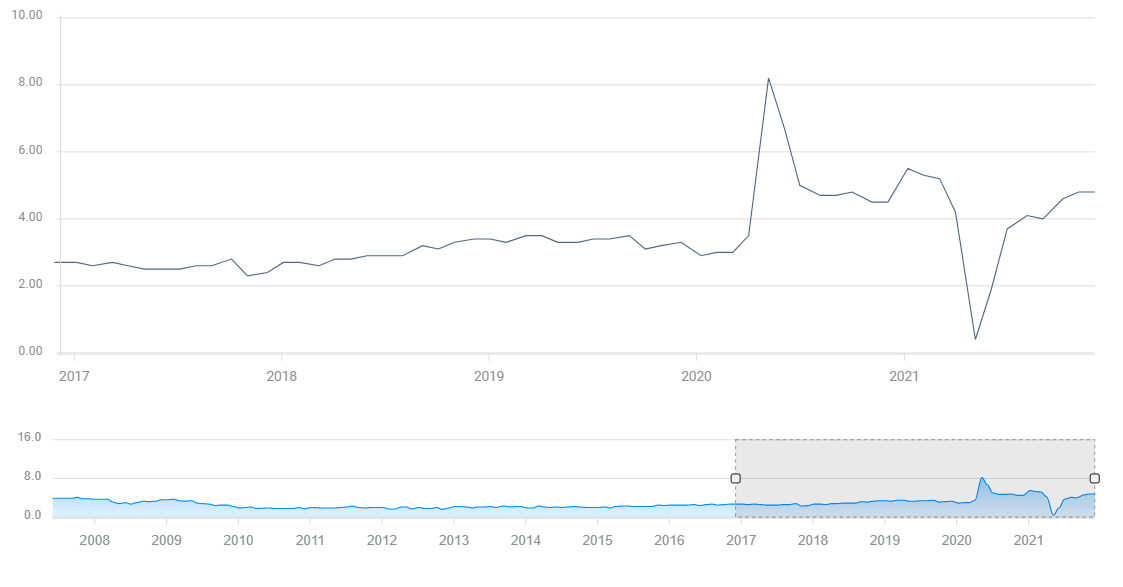

Inflationary pressures are cutting into workers' incomes. Average Hourly Earnings rose 4.8% for the year in November. Inflation, however, was 6.8% higher for the same period. Real wages, income minus inflation, fell 2% in the 12-months to November. Annual wage gains have not been higher than inflation since March.

Average Hourly Earnings

FXStreet

As inflation erodes purchasing power, workers will demand recompense in higher wages. Against a backdrop of widespread labor shortages and employer hiring bonuses, the possibility of a wage spruce spiral moves ever closer.

In this feedback loop, workers ask for and receive wage increases to compensate for rising consumer prices, but those wage hikes are themselves the source of further inflation as they are then passed onto consumers in retail price increases.

Conclusion: The Federal Reserve’s dilemma

Fed officials have abandoned their claim that US inflation is a temporary phenomenon based in the consumer price collapse during the 2020 lockdowns. Blame for the price increase is primarily laid to the shortage of goods produced by supply chain bottlenecks here and overseas and the difficulty of manufacturers to fully staff production in the face of strong consumer demand.

Government spending is another factor that has been largely unmentioned by bank officials. Since the start of the pandemic Federal and state governments have primed the economy with trillions of dollars in spending, much of it as direct grants to consumers and businesses. This liquidity has encountered the extensive and expanding product shortages and helped to drive prices higher.

The Fed’s dilemma is that inflation is easy to spark and difficult to rein in, especially once consumers begin to anticipate price rises. Interest rates have a long lead time for inflation control and it is doubtful that a fed funds tightening cycle beginning in the second half of 2022 will have any impact on inflation before the following year.

What the Fed needs is higher Treasury yields that will bring commercial rates along and begin to curb consumer expectations.

Can the Fed and Chair Jerome Powell execute such a rapid reverse in policy without ravaging its reputation for careful, considered and deliberate transparency?

Fed's Powell was willing to be bold and shock markets in March 2020 as the pandemic took hold. Will it be equally willing now, when the policy change negates its own analysis?

Former Fed Chairman Alan Greenspan, for whom cryptic pronouncements were a policy tool, might have enjoyed the somewhat droll situation.