Stocks try to hold on, as world falls away.

The market closed lower after a prolonged attempt to rally earlier in the day.

There was a very strong 'watch and see' sentiment on Wall Street yesterday. Some adding to their portfolios, with the thought that this will be yet another buying opportunity. What has changed though, is that many were beginning to wonder for the first time, if this economic downturn might set in to become an even scarier more sustained recession. And for the market too.

US Bond yields are again rising. Whereas only a few weeks ago there was a certain confidence that they had peaked. This had been one of the mainstays of the ‘just keep buying’ crowd. The Fed itself is a strident seller of bonds as it reduces it’s balance sheet post Covid.

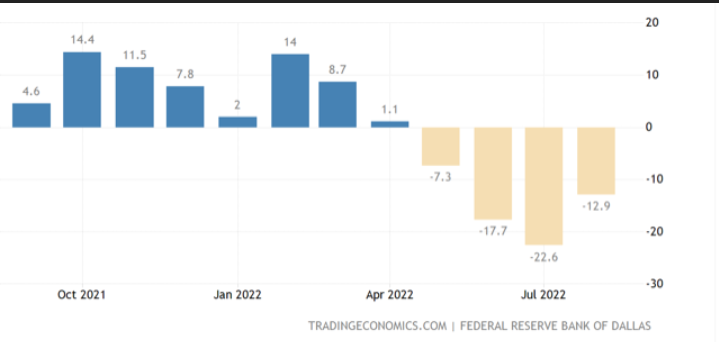

The Dallas Fed Manufacturing Index just registered its fourth month in a row of contraction. Across the nation, factory activity has slowed markedly. The month to month data may bounce around a little bit, but the trend is there for all to see. Retail Sales are flat. Property prices just registered there first monthly decline in three years. Employment is stabilising after a strong post-Covid period. However the number of employers reducing staff numbers is suddenly growing.

What everyone seems to be doing is focussing on what Powell says and does with interest rates. As if that is the only game in town. There use to be a saying “its the economy stupid”. Mostly referring to politics, but Wall Street has tried to drift as far away from this as possible. Even suggesting recessions are good, because that means bond yields will fall. In other words, there is always a reason to buy.

Sounds just a little self-interested doesn’t it.

Companies do well by selling services and goods. This is where the profit comes from to pay investors an appropriate return. If the economy turns down further, regardless of interest rates, from an already significantly weakened position, there may be a sudden convulsion in valuations.

Powell and the Fed are important, but they cannot solve all problems, and have in any case said economic pain is acceptable as they continue to hike.

Higher rates mean higher mortgage stress levels. If property prices were to continue to fall, as I expect, this would be yet another psychic shock to consumers in general. This may very well be the telling indicator for the next 1-3 years as to the state of the US economy.

Recently I raised the “D” word, Depression.

Consumer sentiment is at historic lows. If the consumer becomes any more depressed, so too will the economy. There is a very real risk here, that the USA could experience a depression into 2023. Most of the writing is already on the wall. We just don’t want to see it.

In such circumstances, it is a modest call indeed to suggest the US stock market may fall another 10%, 20%, even 30% over the next 12-18 months.

What could turn it all around?

An immediate end to the Ukraine conflict taking pressure off energy supply and pricing. The Federal Reserve changing its tune to only going to neutral, rather than restrictive levels to fight inflation. A sudden unfathomable end to supply chain disruption. That funds and investors were still not caught long and over-leveraged at the top of the greatest participation in equity market investing in history.

None of the above appear likely any time soon.