Outlook: It’s another big week for data and events, including US CPI on Wednesday and consumer sentiment on Friday. Wednesday also brings two central bank announcements, the RBA (50 bp forecast) and BoC (75 bp expected). Tomorrow it’s the German ZEW.

The inflation rate in the US is likely to go up, not down, temporarily taking attention away from the recession. An especially salient phrase from Sunday TV–"we are talking ourselves into a recession.” In practice, as the nonfarm payrolls showed, we have few signs of it. High probability, maybe, but not here, not yet. Polls show a too-big minority believe we are already in recession. Bloomberg reports, among others, that an Economist/YouGov poll in the middle of June found that 56% believe the US is in a recession. Note that those who believe recession has already struck are more likely Republican than Dems. Maybe because it’s those Dems getting the new jobs. Still, another warning not to give much weight to polls. They can be entertaining but have little value.

Granted, the Atlanta Fed still sees Q2 as a contraction by 1.2%, if better than -1.9% from July 7. The improvement is based on rising personal consumption growth and less negative growth in private investment. That word “growth” is the key clue as to how the Atlanta model words–rates of growth intertwining and goosing and dragging down. It’s a dynamic model and therefore more useful than many others, but still assumes trajectories stay in place, while we chartists know that human conduct does not behave the same as materials in physics–it can veer and stumble on factors never identified. This is why the Atlanta Fed, wisely, updates so often. We get another GDPNow on Friday, July 15.

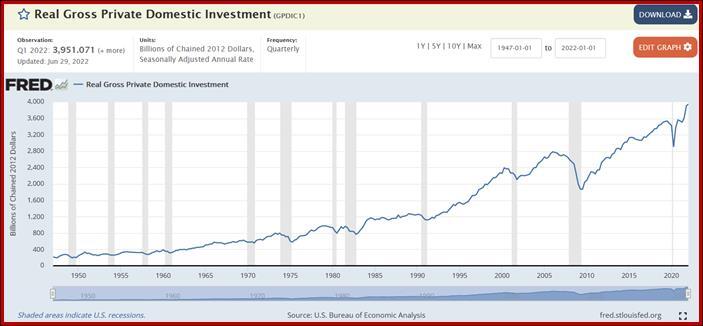

Take “real gross private investment,” a proxy for future output and productivity. It tanked during the pandemic, then soared. In Q1, it grew over 11% y/y. What is it? Business investment in plant and machinery, change in business inventories, and residential construction. We know about the ragged change in inventories due mostly to supply chain issues and some price-gouging, and we know a little about the shortfall in residential construction in part because of mortgage rates (or rather, expectations of even worse mortgage rates). No wonder Q2 is such a mess. Q3 is going to see some of these issues resolved, and by year-end, gross private domestic investment should be nearing “normal,” again.

What is normal? See the splendid Fred chart going back to the 1950’s. The rate of change, i.e., “growth,” can be quite small and still show positive developments in line with the long-term trend. The category may be only about 20% of the US economy–blame the consumer for most of the rest–but it’s also gaining at a rate of about 10-12% y/y, from Q2 2021–pre-Delta, pre-Russian war.

So why are we talking ourselves into recession? Because bad news sell newspapers, as has been the case for millennia. “Dog catches car” is never news.

In the coming week, we see nothing to impede the still-growing consensus that the Fed is on fire, it’s not going to retreat one inch, and damn the torpedoes. In the normal course of events, this keeps the euro on track to hit parity or at least play footsie with it. Sterling will likely bounce if Sunak gets in right away, and the yen is … the yen. No policy change is expected, so that awful diverging return chart should rule.

Here’s the problem–when everything looks clear, that’s exactly when events surprise and shock. So, don’t bet any ranches.

Tidbits: Tomorrow brings another Jan 6 Committee hearing and it promises to be a blockbuster. The ancient Kissinger said on Sunday TV that yes, indeed, this is far worse than Watergate by a mile. At least Nixon was smart and just a crook. He didn’t try to overthrow the Constitution. Also on Tuesday, we get the first photos from the Webb telescope and they promise to be humdingers.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!