- The US Treasury Department is looking to clear up confusion on the new crypto tax reporting requirements.

- The unnamed individual who spoke to Bloomberg said that the Treasury would not go after digital asset companies that do not qualify as a “broker.”

- The guidance from the Treasury is expected to be made public next week.

The United States Treasury Department is looking to clarify the definition of a “broker” in the highly debated infrastructure bill that aims to raise $28 billion in cryptocurrency taxes. According to Bloomberg, new guidance is being prepared to streamline which types of digital asset firms would be subjected to the new reporting requirements.

Treasury to provide clearer crypto tax guidelines

The infrastructure bill passed by the Senate last week had introduced would categorize individuals who are developing blockchain technology and wallets to also report to the Internal Revenue Service (IRS) and cryptocurrency exchanges that act as brokers.

The Treasury Department is now seeking to make it clear that miners and wallet providers would not be subjected to the new reporting requirements as long as they do not provide brokerage services.

According to an unnamed individual who spoke to Bloomberg, the Treasury is further preparing guidance to clarify which cryptocurrency companies would need to comply with the IRS reporting requirements.

The Treasury’s guidance will not provide blanket exemptions based on how the digital asset companies identify themselves but will focus on whether the firm has conducted activity that would qualify as a broker under the tax code.

Currently, the unnamed individual explained that the guidance is being discussed internally but could be made public as soon as next week.

This clarification is an attempt to address the concerns within the cryptocurrency community arising from the $550 billion infrastructure bill that would require crypto firms to report data to the IRS.

Lawmakers that have tried to revise the crypto language in the bill were unsuccessful, as amending the digital asset section would open up the whole legislation to more revisions.

Leading industry advocates, including Coinbase CEO Brian Armstrong, has openly criticized the bill, saying that the government is “trying to pick winners and losers in a nascent industry.”

Elon Musk also added that it was not the time to “pick technology winners or losers,” further commenting that the legislation was hasty.

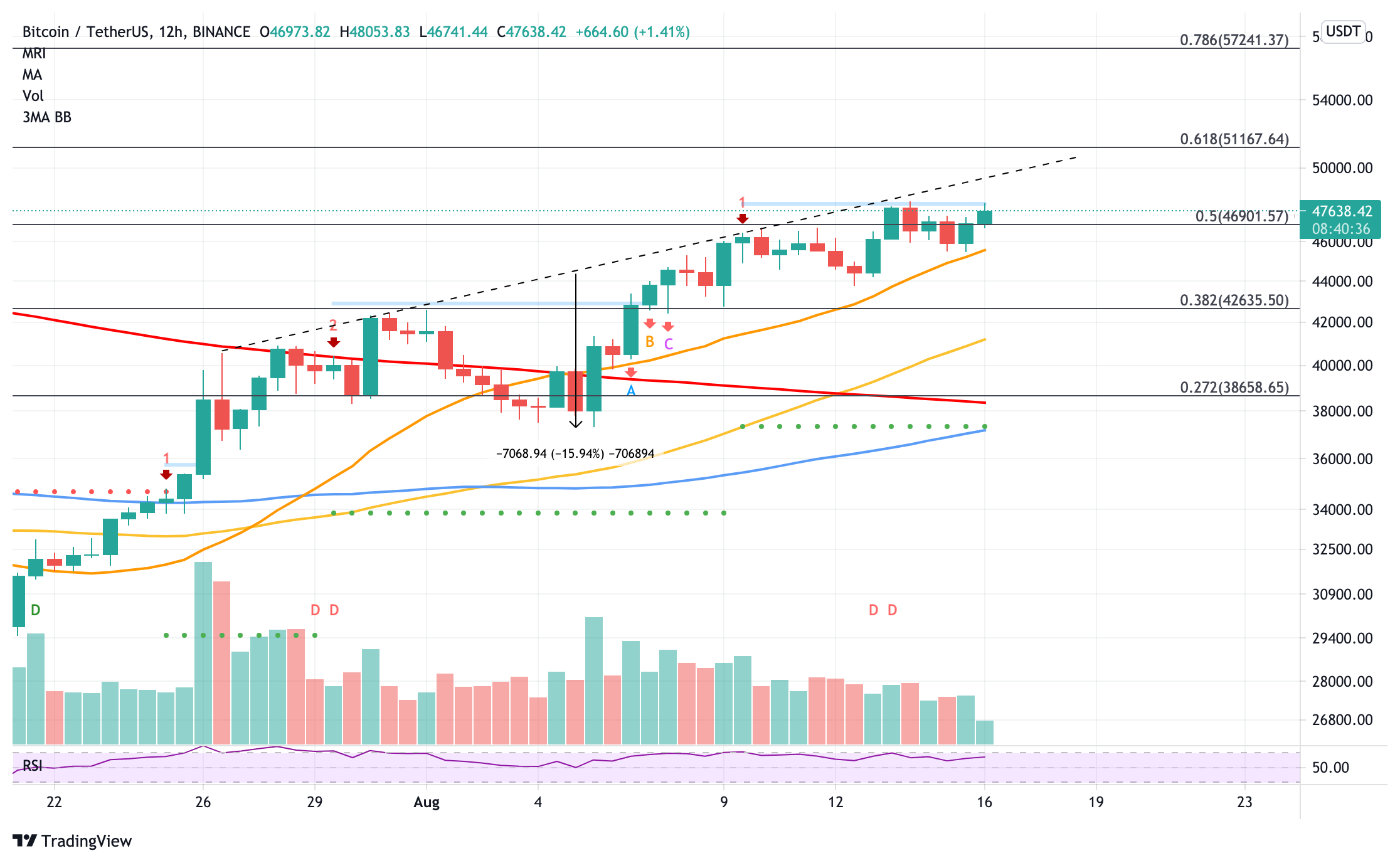

Bitcoin price heads for next hurdle above $47,000

Bitcoin price has surged above $47,000 as it gears up toward facing its next challenge. While continuing to form an inverse head-and-shoulders pattern on the 12-hour chart, BTC is confronted by a resistance line at $47,987 given by the Momentum Reversal Indicator (MRI), which could act as a stiff obstacle for the bellwether cryptocurrency.

For the measured target of the governing technical pattern to materialize, Bitcoin price must slice above the aforementioned resistance level, as well as the neckline of the chart pattern at $49,735 for BTC to target bigger aspirations.

The following hurdle for Bitcoin price appears to be at the 61.8% Fibonacci extension level at $51,167.

BTC/USDT 12-hour chart

Should a confirmation from the Treasury Department regarding the new guidance on crypto tax rules arrive next week, the bulls may also be incentivized to target higher levels.

However, should Bitcoin price witness a reversal of fortune, immediate support arises at the 50% Fibonacci extension level at $46,901, then the 20 twelve-hour Simple Moving Average (SMA) at $45,538.